December 19, 2022

The Markets

Bad news is bad news, once again.

For months, investors have cheered bad economic news. When the United States economy showed signs of weakness, stock markets often reflected investor enthusiasm. The thinking was that bad economic news would persuade the Federal Reserve to slow the pace of rate hikes. Inflation would slide lower, and recession would be avoided.

Last week, there was a shift in attitude.

On Wednesday, the Federal Reserve raised the federal funds rate by half a percent, as expected. Over the course of this year, the fed funds rate has risen from near zero to 4.33 percent. That’s an enormous increase designed to drop inflation by slowing economic growth – and the Fed expects growth to slow.

The dot plot is a chart that reflects the expectations of each member of the Fed’s decision-making committee. It showed that Fed officials expect U.S. economic growth to slow next year. The forecasts indicated gross domestic product (GDP), which is the value of all goods and services produced in the U.S., could grow very slowly or even contract next year (it could contract -0.5 percent or grow to 1.0 percent). Fed officials also anticipated the unemployment rate could rise from a relatively low 3.7 percent to 4.6 percent.

The day after the Fed’s statement, the Commerce Department reported that retail sales declined more than expected in November. That suggests economic growth may be slowing.

The stock market didn’t surge on the bad economic news. It retreated. Vildana Hajric and Lu Wang of Bloomberg reported:

“For the first time in a long time, news that was bad for the economy was bad for the stock market as well, more proof that recession fear has replaced inflation angst as that market’s biggest bugaboo… Rather than rise on speculation that weak data would curb Federal Reserve tightening, the S&P 500 dropped 2.5% on Thursday, while the Nasdaq 100 lost 3.4%. Small-cap stocks lost more than 2.5% and the VIX volatility gauge shot back above 22. The yield on 10-year Treasuries hovered around 3.45%, down from a peak of 3.63% earlier this week.”

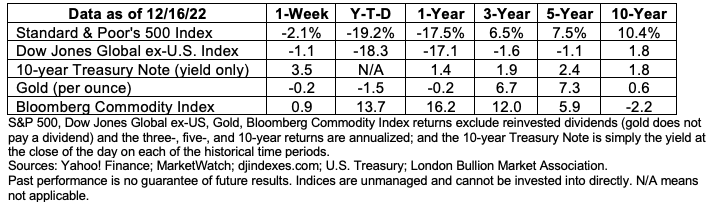

Last week, major U.S. stock indices finished lower, and the Treasury yield curve remained inverted.

We hope you have happy and healthy holidays!

Weekly Focus – Think About It

“I cannot teach anybody anything. I can only make them think.”

—Socrates, philosopher

Required Disclosures:

* These views are those of Carson Coaching, not the presenting Representative, the Representative’s Broker/Dealer, or Registered Investment Advisor, and should not be construed as investment advice.

* This newsletter was prepared by Carson Coaching. Carson Coaching is not affiliated with the named firm or broker/dealer.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* All indexes referenced are unmanaged. The volatility of indexes could be materially different from that of a client’s portfolio. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. You cannot invest directly in an index.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the 3:00 p.m. (London time) gold price as reported by the London Bullion Market Association and is expressed in U.S. Dollars per fine troy ounce. The source for gold data is Federal Reserve Bank of St. Louis (FRED), https://fred.stlouisfed.org/series/GOLDPMGBD228NLBM.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* The Dow Jones Industrial Average (DJIA), commonly known as “The Dow,” is an index representing 30 stock of companies maintained and reviewed by the editors of The Wall Street Journal.

* The NASDAQ Composite is an unmanaged index of securities traded on the NASDAQ system.

* International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage is often obtainable in commodity trading and can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee it is accurate or complete.

* There is no guarantee a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

* Asset allocation does not ensure a profit or protect against a loss.

* Consult your financial professional before making any investment decision.

Sources:

https://www.bloomberg.com/news/articles/2022-12-15/stock-market-traders-discover-that-bad-news-is-bad-after-all (or go to https://resources.carsongroup.com/hubfs/WMC-Source/2022/12-19-22_Bloomberg_Stock%20Market%20Traders%20Discover%20that%20Bad%20News%20is%20Bad%20Afterall_1.pdf)

https://www.newyorkfed.org/markets/reference-rates/effr

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20221214.pdf

https://www.reuters.com/markets/us/us-retail-sales-fall-more-than-expected-november-weekly-jobless-claims-decrease-2022-12-15/

https://www.barrons.com/articles/fed-interest-rates-stock-market-51671240434?refsec=the-trader&mod=topics_the-trader (or go to https://resources.carsongroup.com/hubfs/WMC-Source/2022/12-19-22_Barrons_The%20Fed%20is%20Making%20a%20Mistake%20and%20the%20Stock%20Market%20Will%20Pay_5.pdf)

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value_month=202212

https://www.barrons.com/articles/everyday-decisions-wealth-retirement-annamaria-lusardi-51638573781 (or go to https://resources.carsongroup.com/hubfs/WMC-Source/2022/12-19-22_Barrons_How%20Everyday%20Decisions%20Affect%20Your%20Wealth_7.pdf)

https://gflec.org/wp-content/uploads/2022/04/TIAA-Institute-GFLEC-2022-Personal-Finance-P-Fin-Index.pdf

https://www.goodreads.com/quotes/tag/knowledge

Disclosure – All investment carries risk, and we cannot guarantee performance or results. Past performance does not guarantee future results. GIA does not earn any compensation from any of the non-GIA links provided in these resources. The market insights, podcast, blogs, book recommendations, self improvement thoughts, food recipes and activities are based on our perspectives and experience, and may not apply to your unique situation or be appropriate for your health and wellness. We are not aware of any conflicts of interest relating to any testimonials or endorsements. Please contact us for any questions relating to the content above, or to discuss how we can support you in your specific situation, and help you to reach your financial and personal goals.

Share This Story, Choose Your Platform!

About the Author: Grant Carmichael

Related Posts